Home » Everything You Need to Know About GSTR-2B

- TRENDING ARTICLE

Everything You Need to Know About GSTR-2B

Anurag Mittal

Anurag Mittal, CEO and Co-founder of Olao Books, is an expert in business finance and operations, with a focus on transforming accounting and payroll solutions for small and medium-sized businesses. As the Co-founder and former Head of Operations and Business at Vervotech, Anurag played a pivotal role in driving 10x revenue growth and leading the company to a successful acquisition.

Table of Contents

ToggleSo, What is GSTR-2B?

It’s an auto-generated statement under the Goods and Services Tax (GST) system in India that tells you exactly what input tax credit you’re eligible for. This statement pulls data from what your suppliers have filed in their GST returns (like GSTR-1, GSTR-5, and GSTR-6) and shows up like clockwork on the 14th of every month. The key difference between GSTR-2B and other statements like GSTR-2A? It’s static. It doesn’t change after it’s generated, so you’re working with a consistent set of data every month.

Important things of GSTR-2B that you need to know

Fixed and Unchanging

Unlike GSTR-2A, which keeps updating based on supplier filings, GSTR-2B is a snapshot of your ITC as of a specific date. Think of it like a photograph — once it’s taken, it stays the same. This makes it much easier for you to match your purchase records and plan your ITC claims without the fear that things will shift around.

All-in-One Overview

GSTR-2B gives you a complete view of your available and ineligible ITC, breaking down credits into different heads like IGST, CGST, SGST, and Cess. For example, if you’ve purchased raw materials from different states, GSTR-2B will show how much tax you paid on each transaction under different tax categories.

Relevant to a Specific Month

This statement focuses on a particular period — it covers all the supplier data from the 12th of the previous month to the 11th of the current month. This timeline helps you cross-check everything on a monthly basis. For instance, if you are reconciling your books for July, GSTR-2B for July will capture supplier data submitted up to the 11th of August.

Cases where ITC remains unavailable in GSTR-2B

- If the recipient is located in a different state, even if the place of the supplier & the supply is the same, ITC will remain unavailable.

- If the supplier has not filed their GSTR-1

- If the supplier has not mentioned the transaction details in their GSTR-1

- If the full payment or the goods & services are not received by both or either parties

- If the claim is made after the time-limit defined in section 16(4) of the CGST Act (30th September of the next financial year or the date of filing annual returns)

- If the ITC is ineligible as per any scenarios mentioned in the Blocked ITC Rule

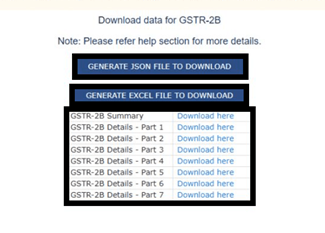

How to View & Download GSTR-2B Reconciliation Data from the GST Portal?

Getting your GSTR-2B is straightforward. Here’s a quick rundown:

Step 1: Log in to the GST Portal: Head to www.gst.gov.in and use your credentials to log in.

Step 2: Go to the Returns Dashboard: Select the right financial year and return period.

Step 3: Download Your GSTR-2B: Click on the ‘GSTR-2B’ option, and voila! You can download it in PDF or Excel format, depending on what works best for you.

Step 4: Take suitable action on the GSTR-2B based on the option chosen in Step 3

- Intend to download: If you plan to download, click on the button known as “Generate JSON File To Download” to check out the statement on Offline Matching Tool. Alternatively, click on the “Generate Excel file to download” button to obtain the data in the excel file on your system.

b) Intend to View:

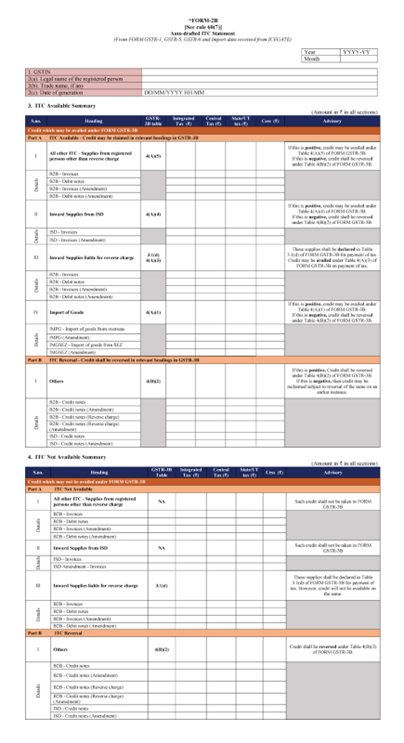

The Summary tab is divided into:

- Part A (ITC Available): Shows the Input Tax Credit (ITC) that is available as of the generation date, categorized into credits that can be availed and those that must be reversed (Table 3).

- Part B (ITC Not Available): Displays the ITC that is not available, further classified into unavailable ITC and ITC reversal (Table 4).

You can access detailed documents by clicking on the hyperlinked texts for B2B invoices, debit notes, and their amendments.

What’s Inside GSTR-2B?

Part A: ITC You Can Claim

- Invoices and Debit Notes: Shows all the ITC available on invoices and debit notes filed by suppliers.

- Imports of Goods and Services: Lists the ITC you can claim on imports.

- Reverse Charge Mechanism (RCM): Details credits available on transactions like purchases from unregistered dealers or certain services where you have to pay tax directly.

Part B: ITC You Can’t Claim

- Blocked Credit under Section 17(5): This is where you find credits you can’t claim, like those on motor vehicle purchases or health services.

- Supplies from Composition Dealers: If you’ve bought goods from a dealer under the composition scheme, those credits will show up here as non-claimable.

- Credit Notes: Lists any credit notes your suppliers have issued, which could reduce your available ITC.

How to Reconcile GSTR-2B with Your Books

Step 1: Match Your Data

Start by comparing the data in your purchase register with what’s in GSTR-2B. Make sure details like the supplier’s GSTIN, invoice number, and tax amount match up. For example, if you bought office supplies in bulk, check if the invoices issued by the supplier reflect correctly in GSTR-2B.

Step 2: Spot the Mismatches

Identify any discrepancies, such as:

- Missing Invoices: Maybe your supplier didn’t file an invoice.

- Different GST Rates: Your supplier charged a different rate than expected.

- Duplicate Entries: Either in your books or the GSTR-2B.

Step 3: Chat with Your Suppliers

If there are mismatches, pick up the phone or send an email to your supplier to sort them out. For instance, if a supplier hasn’t filed GSTR-1 for a purchase you made, a quick nudge from you might be all that’s needed.

Step 4: Fix Your GSTR-3B

Once you’ve reconciled everything, make the necessary adjustments in your GSTR-3B return. For example, if your GSTR-2B shows an eligible ITC of ₹10,000, but you’ve already claimed ₹12,000 in GSTR-3B, you need to adjust the claim accordingly to avoid penalties.

Step 5: Keep All Your Docs Handy

Store all communication, supporting documents, and explanations for discrepancies. These records will be crucial if there’s ever an audit. For example, keeping a screenshot of a chat with a supplier about correcting an invoice can save you a lot of headaches down the line.

The detailed format of GSTR-2B

What is the Difference between GSTR-2A and GSTR-2B?

While similar in purpose to GSTR-2A, GSTR-2B differs in its generation frequency and some additional features.

In the table drawn below, we can learn about the differences in their aspects.

GSTR-2A | GSTR-2B | |

Nature of Return: | GSTR-2A is a dynamic return that constantly updates when invoices are uploaded by suppliers. | GSTR 2B is a static return that is updated every month. |

Frequency | Real Time | Monthly |

Source of Information | GSTR-1/IFF, GSTR-5, GSTR – 7 (GST -TDS), GSTR – 6 (ISD), GSTR – 8 (GST -TCS) | GSTR 2B has sources of information from GSTR- 1/IFF, GSTR-5 (Non-Resident) GSTR – 6 (ISD) |

Additional Information: | GSTR-2A provides a basic overview of ITC based on GSTR-1 data. | GSTR-2B offers a more detailed and categorized breakdown of ITC. |

User Accessibility: | GSTR-2A is available for real-time monitoring and reference during GSTR-3 preparation. | GSTR-2B is designed in a user-friendly format for easy comprehension and reconciliation. |

GSTR-2B vs. GSTR-3B: Reconciling Your Purchase Register

To maintain compliance, taxpayers should regularly reconcile the data in their GSTR-2B with their own records and accounting books. This ensures:

- No Duplicate Input Tax Credit (ITC): ITC should not be claimed more than once for the same transaction.

- Reversals Are Properly Recorded: Any necessary reversals of credit should be accurately reported in GSTR-3B in line with GST regulations.

- Reverse Charge Compliance: Taxes charged on a reverse charge basis must be correctly paid to the government.

- ITC for Paid Taxes Only: Tax credit should only be claimed for taxes actually paid to the supplier.

- Matching of Invoices: Purchase invoices used to claim tax credit in GSTR-3B should match those appearing in GSTR-2B, as required by Section 16 of the CGST Act.

Key Changes in ITC Claims: Before January 1, 2022, taxpayers could provisionally claim 5% of eligible tax credit as per GSTR-2B, under CGST Rule 36(4). However, this provision was removed by amendments in December 2021 (Central Tax Notifications No. 40/2021 and No. 39/2021).

Avoiding Excess Claims: Any excess credit claimed must be repaid with 24% annual interest. Additionally, ITC for a specific financial year must be claimed before the due date for filing GSTR-3B for September of the following year or the annual return filing date, whichever comes first.

Preventing Major Mismatches: It’s essential to avoid discrepancies between GSTR-2B and GSTR-3B, as significant mismatches could result in the cancellation of GST registration.

Why Focus on GSTR-2B? Reconciling GSTR-2B with purchase records is more critical than with GSTR-3B. Since late 2020, GSTR-3B has been auto-populated with values from GSTR-1 and GSTR-2B, reducing the likelihood of errors.

Using the Offline Matching Tool: The GST portal offers an Offline Matching Tool to help taxpayers match their purchase register with GSTR-2B. It’s crucial to upload data in the exact format required by the portal to avoid errors during reconciliation.

Key Matching Parameters: Reconciliation should be based on:

- GSTIN

- Document type, number, and date

- Total taxable value

- Total tax amount (sum of IGST, CGST, SGST, and CESS, if applicable)

- Tax amount per head

Handling Missing Documents: If any invoices or debit notes are missing from GSTR-2B, the taxpayer should immediately contact the supplier to ensure these documents are uploaded in the next GSTR-1 filing. Regular reconciliation is advised, ideally starting from the 14th of the month following the tax period.

Common Causes of Mismatches:

- Different reporting periods between supplier and buyer.

- Debit or credit notes issued by suppliers not accounted for by the buyer.

- Amendments made by suppliers in later GSTR-1 filings, often due to corrections in sales details initially populated by the e-invoicing system.

By regularly matching your records with GSTR-2B and promptly addressing discrepancies, you can ensure smooth GST compliance and avoid penalties.

Conclusion

GSTR-2B can be your best friend when it comes to managing your GST compliance. By giving you a consistent, reliable snapshot of your input tax credits each month, it makes reconciliation a lot simpler. Keep a close eye on it, communicate with your suppliers regularly, and make sure all your paperwork is in order. This way, you’ll ensure you’re claiming the right amount of ITC and staying on the right side of the law!

- So, What is GSTR-2B?

- Important things of GSTR-2B that you need to know

- Cases where ITC remains unavailable in GSTR-2B

- How to View & Download GSTR-2B Reconciliation Data from the GST Portal?

- What’s Inside GSTR-2B?

- How to Reconcile GSTR-2B with Your Books

- The detailed format of GSTR-2B

- What is the Difference between GSTR-2A and GSTR-2B?

- GSTR-2B vs. GSTR-3B: Reconciling Your Purchase Register

- Conclusion

Table of Contents

- So, What is GSTR-2B?

- Important things of GSTR-2B that you need to know

- Cases where ITC remains unavailable in GSTR-2B

- How to View & Download GSTR-2B Reconciliation Data from the GST Portal?

- What’s Inside GSTR-2B?

- How to Reconcile GSTR-2B with Your Books

- The detailed format of GSTR-2B

- What is the Difference between GSTR-2A and GSTR-2B?

- GSTR-2B vs. GSTR-3B: Reconciling Your Purchase Register

- Conclusion

Start using OLAO today

- Get Paid Faster. Boost Cash Flow

- Powerful, automated core accounting

- Hands-free bank reconciliation

Frequently Asked Questions

GSTR-2B is a static monthly ITC statement, while GSTR-2A is dynamic and updates in real-time with supplier data.

It is generated on the 14th of each month, covering data from the 12th of the previous month to the 11th of the current month.

Log in to the GST portal, go to the Returns Dashboard, select the period, and click on ‘GSTR-2B’ to download.

ITC may be unavailable if the supplier hasn't filed GSTR-1, details are incorrect, payment isn't made, or claims are late.

Regular reconciliation ensures accurate ITC claims, compliance, and avoids penalties due to mismatches.