Home » GSTR-1 Filing Guide: Compliance Tips 2024, Step by Step guide, Format, Late Fees, Eligibility & Rules, Due Date

- TRENDING ARTICLE

GSTR-1 Filing Guide: Compliance Tips 2024, Step by Step guide, Format, Late Fees, Eligibility & Rules, Due Date

Anurag Mittal

Anurag Mittal, CEO and Co-founder of Olao Books, is an expert in business finance and operations, with a focus on transforming accounting and payroll solutions for small and medium-sized businesses. As the Co-founder and former Head of Operations and Business at Vervotech, Anurag played a pivotal role in driving 10x revenue growth and leading the company to a successful acquisition.

Filing GSTR-1 is a vital task for businesses under the GST system. This guide will walk you through the basics, recent updates, and essential tips for filing GSTR-1 in 2024. Let’s make GSTR-1 filing easy and hassle-free.

Latest Updates on GSTR-1A

22nd June 2024

In the 53rd GST Council meeting, the GST Council recommended that a new optional facility in Form GSTR-1A will be introduced for taxpayers to add/amend details filed in the GSTR-1 (or IFF) for a tax period before filing their GSTR-3B for the same tax period.

Table of Contents

ToggleWhat is GSTR-1?

GSTR-1 is a monthly or quarterly return that should be filed by every registered GST taxpayer, except a few as given in further sections. It contains details of all outward supplies i.e sales. The return has a total of 15 sections, listed down as follows:

- Tables 1, 2 & 3: GSTIN, legal and trade names, and aggregate turnover in the previous year

- Table 4: Taxable outward supplies to registered persons (including UIN-holders) excluding zero-rated supplies and deemed exports

- Table 5: Taxable outward inter-state supplies to unregistered persons where the invoice value is more than Rs.2.5 lakh

- Table 6: Zero-rated supplies as well as deemed exports

- Table 7: Taxable supplies to unregistered persons other than the supplies covered in table 5 (net of debit notes and credit notes)

- Table 8: Outward supplies that are nil rated, exempted and non-GST in nature

- Table 9: Amendments to outward supplies that are taxable and reported in table 4,5 & 6 of the earlier tax periods’ GSTR-1 return (including debit notes, credit notes, refund vouchers issued during the current period)

- Table 10: Debit note and credit note issued to unregistered person

- Table 11: Details of advances received or adjusted in the current tax period or amendments of the information reported in the earlier tax period.

- Table 12: Outward supplies summary based on HSN codes

- Table 13: Documents issued during the period.

- Table 14: For suppliers – Reporting ECO operators’ GSTIN-wise sales through e-commerce operators on which e-commerce operators are liable to collect TCS u/s 52 or liable to pay tax u/s 9(5) of the CGST Act

- Table 14A: For suppliers – Amendments to Table 14

- Table 15: For e-commerce operators – Reporting both B2B and B2C, suppliers’ GSTIN-wise sales through e-commerce operators on which e-commerce operator must deposit TCS u/s 9(5) of the CGST Act

- Table 15A: For e-commerce operators –

Table 15A I – Amendments to Table 15 for sales to GST registered persons (B2B)

Table 15A II – Amendments to Table 15 for sales to unregistered persons (B2C)

Who Should File GSTR 1?

GSTR 1 must be filed by every registered taxpayer. It has to be filed even if the taxpayer has had no transactions in a month.

Registered individuals who do not have to file this form include :

- Taxpayers liable to collect TDS.

- Those liable to collect TCS.

- Suppliers of Online Information Database Access and Retrieval (OIDAR) services (as per Section 14 of the IGST Act).

- Non-resident taxable persons.

- Taxpayers registered under the GST composition scheme.

- Input Service Distributors (ISDs).

Understanding GSTR-1 Filing Process

Importance of GSTR-1 Filing

GSTR-1 is a monthly GST return that contains details of all outward supplies. Filing GSTR-1 accurately is crucial for businesses to ensure compliance with GST regulations. It helps in maintaining transparency and avoiding penalties.

GSTR-1 Filing due date

The due dates for GSTR-1 are based on your aggregate turnover.

Businesses with sales of up to Rs.5 crore have an option to file quarterly returns under the QRMP scheme and are due by the 13th of the month following the relevant quarter.

Whereas, those taxpayers who do not opt for the QRMP scheme or have a total turnover above Rs.5 crore must file the return every month on or before the 11th of the next month.

GSTR-1 Filing late fees and penalty

The following table explains the late fee to be charged (for other than nil GSTR-1 filing cases):

Name of the Act | Late fees for every day of delay | Maximum late fee |

|

|

CGST Act, 2017 | Rs 25 | Rs 1,000 | Rs 2,500 | Rs 5,000 |

Respective SCGT Act, 2017 / UTGST Act, 2017 | Rs 25 | Rs 1,000 | Rs 2,500 | Rs 5,000 |

Total late fees to be paid | Rs 50 | Rs 2,000 | Rs 5,000 | Rs 10,000 |

The following table explains the late fee to be charged (for other than nil GSTR-1 filing cases):

Name of the Act | Late fees for every day of delay | Maximum late fee |

CGST Act, 2017 | Rs 10 | Rs 250 |

Respective SCGT Act, 2017 / UTGST Act, 2017 | Rs 10 | Rs 250 |

Total late fees to be paid | Rs 20 | Rs 500 |

The original late fees used to be Rs.100 per day under each CGST Act and respective SGST/ UTGST Act. Also, the original late fee for Nil return filers used to be Rs.25 per day under each CGST Act and respective SGST/ UTGST Act.

However, CBIC has notified reduced late fees to provide relief for businesses having difficulties in GST return filing.

Also, the CBIC issued notification 20/2021 dated 1st June 2021, to cap the maximum late fee chargeable from June 2021 onwards.

The following table explains the late fee to be charged in case of nil GSTR-1 filing:

Common Mistakes to Avoid in GSTR-1 Filing

To file GSTR-1, you need several documents:

- Invoices for all sales

- Debit and credit notes

- Details of any advances received

- HSN codes for goods and services

Remember, accuracy in filing is key to smooth GST compliance.

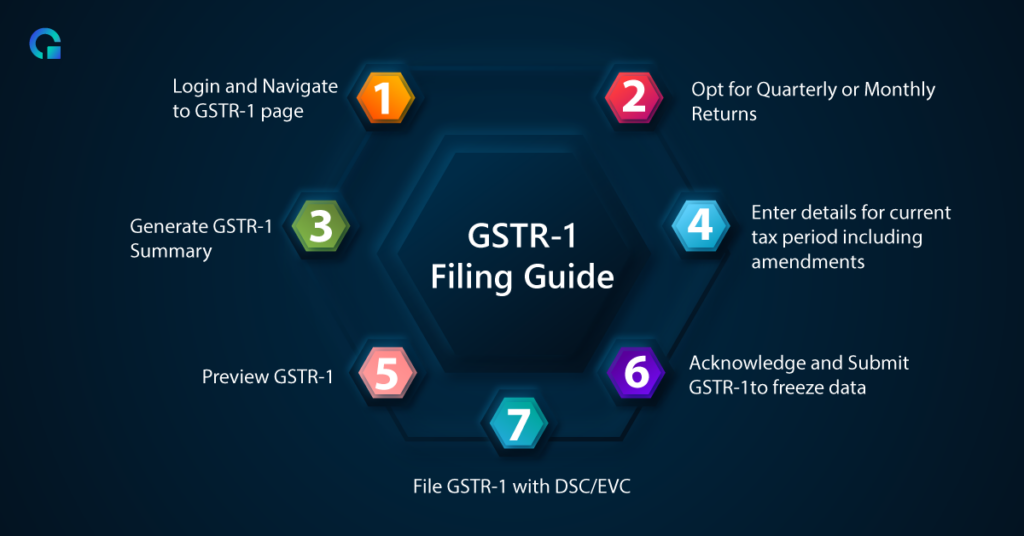

Step-by-Step Guide to GSTR-1 Filing

Filing GSTR-1 can seem daunting, but breaking it down into simple steps makes it manageable. This guide will walk you through the process, ensuring you meet all requirements and avoid common pitfalls.

Eligibility Criteria

Before you start, ensure you meet the eligibility criteria as mentioned in above sections for filing GSTR-1. Generally, any registered taxpayer involved in the supply of goods or services must file this return. However, there are exceptions, such as composition scheme taxpayers and input service distributors.

- Log in to the GST portal using your credentials.

- Navigate to the ‘Services’ section and click on ‘Returns’ and then ‘Returns Dashboard.’

- Select the financial year and return filing period.

- Click on ‘Prepare Online’ under GSTR-1.

- Fill in the required details in the various sections, such as outward supplies, B2B invoices, and B2C invoices.

- Review the information carefully to ensure accuracy.

- Click ‘Submit’ to save the data.

- Once submitted, click on ‘File GSTR-1’ to proceed.

- Sign the form digitally using a Digital Signature Certificate (DSC) or an Electronic Verification Code (EVC).

- After filing, note down the Acknowledgement Reference Number (ARN) for future reference.

Remember, accuracy is crucial in GSTR-1 filing to avoid penalties and ensure smooth processing. Double-check all entries before submission.

By following these steps, you can file your GSTR-1 return efficiently and accurately, ensuring compliance with GST regulations.

Tips for Accurate GSTR-1 Filing

Maintaining Proper Records

Keeping detailed records is crucial for accuracy in tax filing. Ensure that all sales transactions are recorded correctly, including the nature of supplies, tax rates, and applicable taxes. This helps in creating a reliable database for calculating tax liabilities and smooth tax administration.

Utilizing GST Software Effectively

Using GST software can simplify the filing process. It helps in organizing data, reducing errors, and ensuring timely submission. Make sure to choose software that meets your business needs and provides regular updates to comply with changes in GST laws.

Reconciling Sales and Invoices

Regular reconciliation of sales and invoices is essential to avoid discrepancies. This ensures that all transactions are correctly reported, reducing the risk of errors in GST returns. Optimal ITC claims can be achieved by reconciling data accurately.

Timely and accurate GSTR-1 filing helps avoid unnecessary scrutiny or audits from tax authorities, saving businesses from potential penalties and hassles.

Compliance Guidelines for GSTR-1 Filing

Compliance with the rules and regulations of filing tax is extremely necessary. Hence, be aware of any kind of changes that take place in filing the return for GSTR-1. Ensure that each and every employee and you are aware of the changes in the rules and regulations. Encourage employees to report any kind of issues that might crop up during the filing of the GST return. In order to improve compliance, ensure internal audits are being done continuously which will help in finding out the gaps of compliance.

Timely Submission of GSTR-1

Timely filing of GSTR-1 is crucial for GST compliance and sales reporting. The last date to file the GSTR-1 form should be kept in check, for taxpayers. Missing the deadline can lead to penalties and interest charges. To avoid this, set reminders and maintain a calendar of important dates.

Accuracy in Reporting Taxable Supplies

Accurate reporting of all outward supply transactions is mandatory for all registered taxpayers. GSTR-1 data is used to auto-populate other GST forms and calculate taxable liability in GSTR-3B. Discrepancies between GSTR-1 and GSTR-3B can result in scrutiny and audits. Double-check all entries to ensure they match your sales records.

Adherence to GST Rules and Regulations

Stay updated with any changes in GST laws that impact GSTR-1 filing. Regularly review the GST portal and official notifications. Conduct internal audits to identify and rectify compliance gaps. Encourage employees to report any issues they encounter during the filing process. This proactive approach helps in maintaining compliance and avoiding legal complications.

Challenges in GSTR-1 Filing

Data Reconciliation Issues

One of the main challenges in GSTR-1 filing is data reconciliation. Ensuring that the sales data matches with the invoices can be a daunting task. Any mismatch can lead to discrepancies, which might result in penalties or further scrutiny from tax authorities.

Complexity of Input Tax Credit

The process of claiming Input Tax Credit (ITC) is quite complex. Taxpayers need to ensure that all the details are accurate and that they comply with the GST rules. Mistakes in ITC claims can lead to significant financial losses and legal issues.

Changes in GST Laws Impacting GSTR-1

The GST laws are frequently updated, and these changes can impact the GSTR-1 filing process. For instance, the presentation or layout of GSTR-1 has changed over time, making it more user-friendly. However, keeping up with these changes requires constant attention and adaptation. Additionally, the GSTR-1 deadline can sometimes be extended, adding another layer of complexity to the filing process.

Staying updated with the latest GST laws and guidelines is crucial for accurate GSTR-1 filing. Regular training and consultation with tax experts can help mitigate these challenges.

Conclusion

Filing GSTR-1 accurately and on time is essential for businesses to stay compliant with GST regulations. By understanding the process, maintaining proper records, and using the right tools, businesses can avoid common mistakes and ensure smooth filing. Regular training and consulting with tax experts can further enhance compliance. As GST laws continue to evolve, staying updated and adapting to changes will be crucial. With the tips and guidelines provided in this guide, businesses can navigate the complexities of GSTR-1 filing with confidence and ease.

Table of Contents

- What is GSTR-1?

- Who Should File GSTR 1?

- Understanding GSTR-1 Filing Process

- GSTR-1 Filing late fees and penalty

- Common Mistakes to Avoid in GSTR-1 Filing

- Step-by-Step Guide to GSTR-1 Filing

- Tips for Accurate GSTR-1 Filing

- Compliance Guidelines for GSTR-1 Filing

- Challenges in GSTR-1 Filing

- Conclusion

Start using OLAO today

- Get Paid Faster. Boost Cash Flow

- Powerful, automated core accounting

- Hands-free bank reconciliation

Frequently Asked Questions

GSTR-1 is a monthly or quarterly return that summarizes a taxpayer’s sales. It is essential for GST compliance.

All registered taxpayers, except composition vendors, those with Unique Identification Numbers, and non-resident foreign taxpayers, need to file GSTR-1.

The GSTR-1 is due on the 13th of the month following the reporting period. For quarterly filers, it's due on the 13th of the month after the quarter ends.

Yes, you can make amendments to your GSTR-1, but there are specific details that have restrictions on changes.

If you don't file GSTR-1 on time, you may incur a late fee of Rs 500 (Rs 250 for CGST and Rs 250 for SGST).

To avoid common mistakes, ensure you maintain proper records, use GST software effectively, and reconcile sales and invoices regularly.

Yes, GSTR-1 can be filed after filing GSTR-3B as it provides details of outward supplies, which can be furnished later. However, timely filing of GSTR-1 is crucial for reconciling data with recipients. It is recommended to adhere to the due dates for both returns to ensure compliance with GST regulations.