Home » DRC-01C Intimation under Rule 88D: Resolving ITC Mismatches Between GSTR-2B and GSTR-3B

- TRENDING ARTICLE

DRC-01C Intimation under Rule 88D: Resolving ITC Mismatches Between GSTR-2B and GSTR-3B

Anurag Mittal

Anurag Mittal, CEO and Co-founder of Olao Books, is an expert in business finance and operations, with a focus on transforming accounting and payroll solutions for small and medium-sized businesses. As the Co-founder and former Head of Operations and Business at Vervotech, Anurag played a pivotal role in driving 10x revenue growth and leading the company to a successful acquisition.

When it comes to GST compliance in India, one of the key challenges businesses face is managing their Input Tax Credit (ITC) correctly. Rule 88D of the Central Goods and Services Tax (CGST) Act is designed to help businesses do just that by addressing discrepancies between the ITC available in GSTR-2B and the ITC claimed in GSTR-3B. Let’s break down what Rule 88D is, why it matters, and how to handle any mismatches like a pro.

Table of Contents

ToggleWhat is Rule 88D of CGST?

Rule 88D is essentially a rule that requires you to reconcile any differences between the ITC (Input Tax Credit) shown in GSTR-2B and the ITC you actually claimed in GSTR-3B.

Think of GSTR-2B as a monthly statement that shows the ITC available to you, based on the returns filed by your suppliers (like GSTR-1, GSTR-5, and GSTR-6). Meanwhile, GSTR-3B is the summary return that you file yourself, declaring your tax liabilities, including the ITC you’ve claimed.

Why is Rule 88D Important?

Rule 88D plays a crucial role in keeping the GST system fair and transparent by ensuring that ITC claims are accurate and match what your suppliers report. This helps to:

- Prevent Wrongful ITC Claims: By catching discrepancies early, it reduces the risk of claiming credits you’re not entitled to.

- Reduce Litigation and Penalties: A mismatch can lead to scrutiny, interest, or penalties. Rule 88D prompts you to fix these issues proactively.

- Streamline the Tax Process: Ensures that the overall tax process remains smooth, minimizing disputes between taxpayers and the tax authorities.

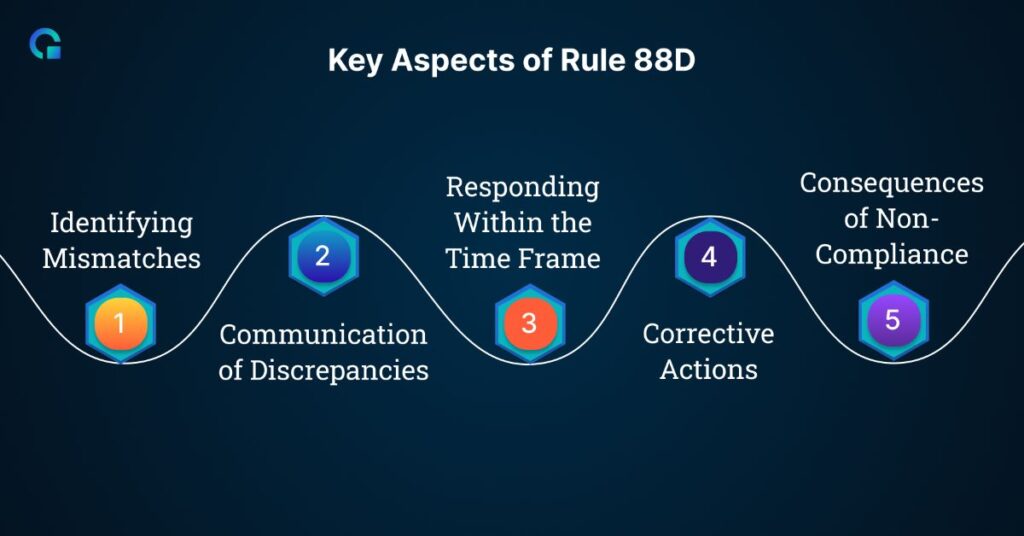

Key Aspects of Rule 88D

1. Identifying Mismatches

The GST system automatically flags any differences between the ITC claimed in GSTR-3B and what’s available in GSTR-2B. For instance, if your supplier hasn’t filed their GSTR-1 properly, the credits available to you in GSTR-2B might be lower than what you claimed in GSTR-3B.

2. Communication of Discrepancies

Once a mismatch is detected, the GST system sends you an automated notice to reconcile the differences. Think of this as a nudge to either correct the discrepancies or provide a valid explanation.

3. Responding Within the Time Frame

You need to respond to the notice within a specified period. Ignoring it can lead to penalties or even more scrutiny.

4. Corrective Actions

If you agree with the discrepancy, you should make the necessary corrections in your next GSTR-3B filing. If you disagree, you’ll need to provide a valid reason or supporting documents to justify your claim.

5. Consequences of Non-Compliance

Failing to comply with Rule 88D can have serious consequences, including:

- Penalties and Interest Charges: For delays or inaccuracies.

- GST Registration Cancellation: In extreme cases of non-compliance.

- Impact on Compliance Rating: A poor compliance rating can affect your business reputation and operations.

Steps to Handle ITC Mismatches Under Rule 88D

1. Regular Reconciliation

Make it a habit to reconcile your books with GSTR-2B and GSTR-3B regularly. This helps catch any discrepancies early. Many businesses use automated tools or software for this to save time and reduce errors.

2. Monitor ITC Availability

Keep an eye on your suppliers to ensure they file their GSTR-1 returns correctly and on time. If your suppliers delay or make mistakes in their filings, it directly impacts the ITC available to you in GSTR-2B.

3. Respond Promptly to Notices

If you receive a notice about an ITC mismatch, don’t delay. Quickly gather all necessary documents, like invoices and payment records, and provide detailed justifications if you believe your ITC claim is correct.

4. Use the Matching Tool on the GST Portal

Leverage the matching tool provided on the GST portal to identify discrepancies before you file. This proactive approach can save you from headaches later.

Best Practices for Staying Compliant with Rule 88D

1. Keep Accurate Records

Maintain detailed records of all transactions, invoices, and communications with suppliers to support your ITC claims.

2. Conduct Regular Audits

Periodically check that your ITC claims match what’s reported in GSTR-2B and GSTR-3B. This proactive step can catch errors early.

3. Stay Updated with GST Rules

GST laws and rules can change, so keep yourself informed about any updates or amendments to ensure ongoing compliance.

4. Educate Your Team

Make sure your finance and accounting teams understand the importance of compliance, especially around ITC claims, and know how to handle discrepancies.

Conclusion

Rule 88D is a vital tool for ensuring that businesses report and claim ITC accurately under GST. By understanding and following this rule, you can avoid penalties, maintain smooth operations, and ensure your business stays on the right side of the law. Regular reconciliation, prompt responses to notices, and diligent record-keeping are key to navigating Rule 88D effectively.

Start using OLAO today

- Get Paid Faster. Boost Cash Flow

- Powerful, automated core accounting

- Hands-free bank reconciliation

Frequently Asked Questions

Rule 88D of the CGST Act mandates the reconciliation of discrepancies between the Input Tax Credit (ITC) available in GSTR-2B and the ITC claimed in GSTR-3B to ensure accurate GST reporting.

ITC mismatches can be identified by regularly reconciling your ITC claims with the ITC reflected in GSTR-2B. The GST portal also flags discrepancies and sends automated notices if mismatches are detected.

Non-compliance with Rule 88D can lead to penalties, interest charges, cancellation of GST registration, and a negative impact on your compliance rating.

Businesses can avoid ITC mismatches by regularly reconciling their GSTR-2B and GSTR-3B, monitoring supplier filings, maintaining accurate records, and promptly responding to any GST notices.

To respond to an ITC mismatch notice, you must provide a valid explanation or supporting documents to justify your ITC claims or make corrections in your next GSTR-3B filing within the specified timeframe.