Home » What is the Reverse Charge Mechanism (RCM) in GST?

- TRENDING ARTICLE

What is the Reverse Charge Mechanism (RCM) in GST?

Anurag Mittal

Anurag Mittal, CEO and Co-founder of Olao Books, is an expert in business finance and operations, with a focus on transforming accounting and payroll solutions for small and medium-sized businesses. As the Co-founder and former Head of Operations and Business at Vervotech, Anurag played a pivotal role in driving 10x revenue growth and leading the company to a successful acquisition.

Table of Contents

ToggleLatest updates

23rd July 2024

In the Union Budget 2024, the Finance Minister proposed an amendment to Section 13 of the CGST Act to provide for the time of supply of services where the invoice is required to be issued by the recipient of services in cases of reverse charge supplies from the unregistered supplier.

*This will come into force once notified by the CBIC.

26th June 2024

The CBIC had issued the circular no. 211/5/2024-GST dt 26th June 2024 to clarify the recommendation by the GST Council w.r.t the availing of input tax credit under the provisions of section 16(4) of CGST Act for which the recipient has issued the invoice under RCM.

22nd June 2024

In the 53rd GST Council meeting held on 22nd June 2024, the Council recommended clarifying that in cases of supplies received from unregistered suppliers, where tax has to be paid by the recipient under reverse charge mechanism (RCM), and invoice is to be issued by the recipient only, the relevant financial year for calculation of time limit for availing of input tax credit under the provisions of section 16(4) of CGST Act is the financial year in which the recipient has issued the invoice.

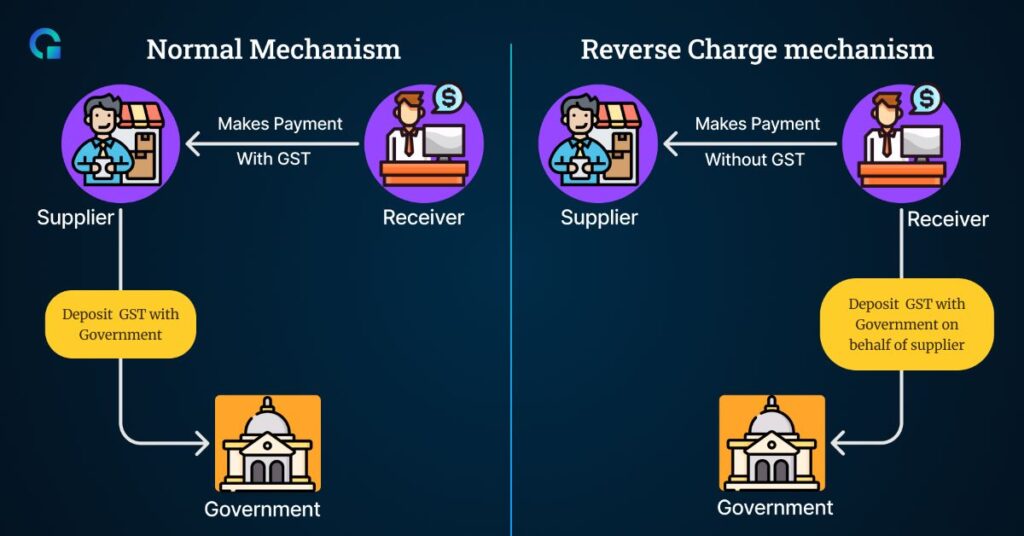

Under the Goods and Services Tax (GST) system, the Reverse Charge Mechanism (RCM) flips the usual way GST is paid. Typically, the seller of goods or services collects GST from the buyer and then pays it to the government. But with RCM, this responsibility shifts to the buyer. This change was made to widen the tax net, reduce evasion, and boost compliance.

When Does Reverse Charge Apply?

RCM kicks in under certain conditions:

- Specified Goods and Services: The government has a list of goods and services where RCM automatically applies. For instance, if you hire a lawyer for legal services or use a goods transport agency, RCM applies. Similarly, if a registered business buys from an unregistered supplier, the buyer must pay GST under RCM.

- Purchases from Unregistered Dealers: When a registered dealer buys goods or services from an unregistered supplier, RCM comes into play.

- Services from Foreign Entities: If you receive services from a foreign entity that doesn’t have an office in India, you, as the recipient, are liable to pay GST under RCM.

- Transactions Under Section 9(4) of the CGST Act: Any goods or services received from an unregistered person shift the GST liability to the recipient.

Types of Supplies Covered Under RCM

RCM applies to both goods and services. Here’s a breakdown:

1. Goods:

- Cashew nuts (not shelled or peeled)

- Tobacco leaves

- Silk yarn

- Lottery tickets (supplied by a state government)

- Used vehicles (from an unregistered person)

- Alcoholic liquor for human consumption (supplied by an unregistered person)

2. Services:

- Legal services provided by an individual advocate or senior advocate.

- Transport services provided by a goods transport agency.

- Sponsorship services provided to any corporate body or partnership firm.

- Directors’ services provided by a company director.

- Security services provided by an agency to a registered person.

What Are the Responsibilities of the Recipient Under RCM?

When you’re the buyer under RCM, here’s what you need to do:

- Pay GST Directly: You must pay GST (CGST + SGST for intra-state or IGST for inter-state) directly to the government.

- Issue a Self-Invoice: If you buy from an unregistered supplier, you must issue an invoice to yourself.

- Maintain Records: Keep detailed records of all transactions where RCM applies. This includes the supply details, tax rates, the amount payable, and the date.

- Claim Input Tax Credit (ITC): You can claim input tax credit (ITC) for the tax you paid under RCM, provided you use those goods or services for business purposes and meet other ITC conditions.

How to Calculate GST Under Reverse Charge?

To compute the GST liability under RCM, use this simple formula:

GST Liability=Value of Supply×Applicable GST Rate\text{GST Liability} = \text{Value of Supply} \times \text{Applicable GST Rate}GST Liability=Value of Supply×Applicable GST Rate

For example, if you purchased goods worth ₹10,000 that are subject to an 18% GST rate, your GST liability under RCM would be:

GST Liability=10,000×0.18=₹1,800\text{GST Liability} = 10,000 \times 0.18 = ₹1,800GST Liability=10,000×0.18=₹1,800

You must pay this amount to the government by the due date for filing your GST return.

Filing Requirements and Compliance

1. Form GSTR-3B:

Report your tax liability under RCM in Form GSTR-3B, a monthly self-declaration form. Include:

- Taxable value of inward supplies liable to reverse charge.

- The GST amount payable.

- The Input Tax Credit (ITC) you’re claiming.

2. Annual Return:

Include all RCM-related details in the annual return (Form GSTR-9). This should cover the total taxable value, GST paid, and ITC claimed under RCM.

Penalties for Non-Compliance

Not complying with RCM rules can lead to penalties for non-compliance including:

- Late Fees: ₹20 per day (₹10 for CGST and ₹10 for SGST), up to a maximum of ₹5,000.

- Interest: 18% per annum on any outstanding tax amount from the due date until payment.

- Further Penal Actions: Repeated violations could lead to heavier fines or legal proceedings.

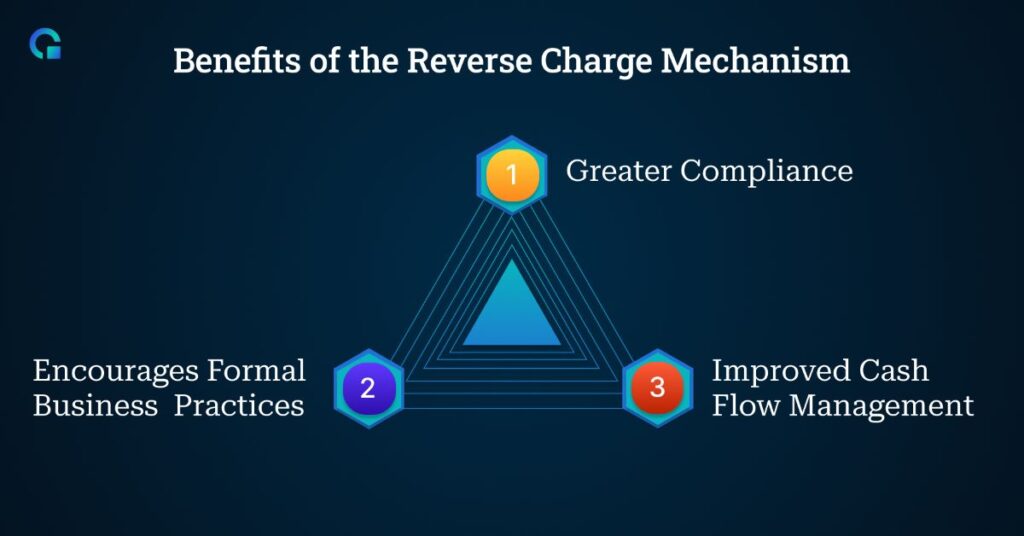

Benefits of the Reverse Charge Mechanism

- Greater Compliance: By shifting tax liability to the buyer, the government broadens the tax base and reduces evasion.

- Encourages Formal Business Practices: The requirement to deal with registered suppliers fosters more formal business activities.

- Improved Cash Flow Management: Since businesses can claim ITC for the tax paid under RCM, they can better manage their cash flows by offsetting liabilities against eligible credits.

Conclusion

Understanding the Reverse Charge Mechanism under GST is essential for businesses to stay compliant and avoid penalties. By following the rules, businesses can benefit from smoother transactions, better cash flow management, and reduced tax liability. Keep up-to-date with any changes to RCM to navigate the GST framework effectively.

Table of Contents

Start using OLAO today

- Get Paid Faster. Boost Cash Flow

- Powerful, automated core accounting

- Hands-free bank reconciliation

Frequently Asked Questions

RCM shifts GST payment responsibility from the supplier to the recipient for specific goods or services.

RCM applies to specified services, purchases from unregistered suppliers, or foreign entities.

Yes, if the goods or services are for business use and meet ITC conditions.

Multiply the supply value by the applicable GST rate (e.g., ₹10,000 x 18% = ₹1,800).

Penalties include late fees, interest at 18% per annum, and possible legal action.