Home » Mastering the Place of Supply Under GST: A Comprehensive Guide with Real-Life Examples

- TRENDING ARTICLE

Mastering the Place of Supply Under GST: A Comprehensive Guide with Real-Life Examples

Anurag Mittal

Anurag Mittal, CEO and Co-founder of Olao Books, is an expert in business finance and operations, with a focus on transforming accounting and payroll solutions for small and medium-sized businesses. As the Co-founder and former Head of Operations and Business at Vervotech, Anurag played a pivotal role in driving 10x revenue growth and leading the company to a successful acquisition.

Have you ever found yourself tangled in the complexities of GST, especially when it comes to figuring out the “Place of Supply”? You’re not alone! Many business owners and professionals grapple with this concept, which is crucial for determining the right type of GST to apply to transactions.

In this guide, we’ll demystify the Place of Supply under GST with simple explanations and real-life examples. By the end, you’ll have a clear understanding of how it works and how to apply it correctly in your business dealings.

Table of Contents

ToggleWhy is Place of Supply Important?

Before diving into the specifics, let’s understand why the Place of Supply matters:

- Determines Tax Type: It helps decide whether a transaction is intra-state (CGST and SGST) or inter-state (IGST).

- Affects Tax Revenue Distribution: Ensures the correct state receives the tax revenue.

- Impacts Input Tax Credit (ITC): Incorrect determination can lead to ITC mismatches and compliance issues.

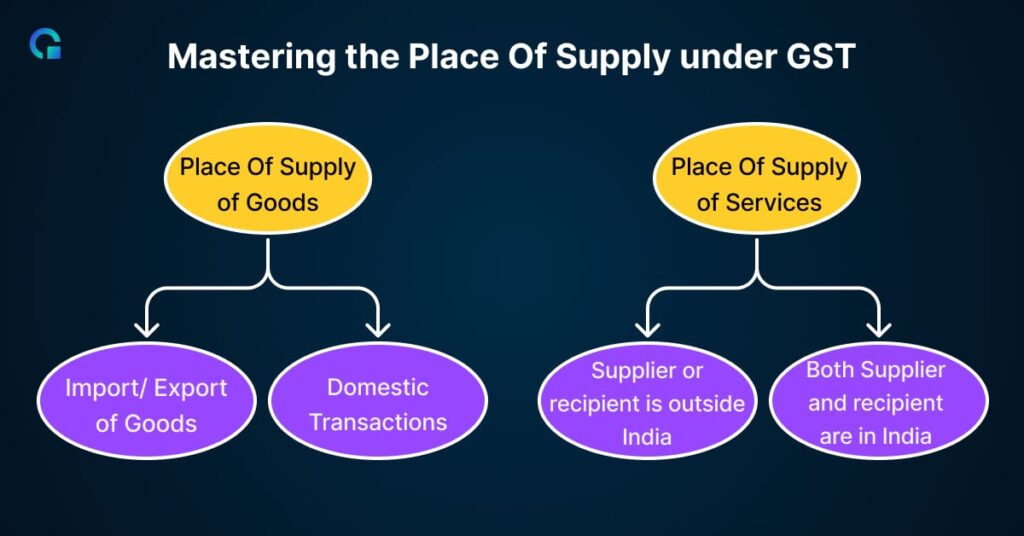

Place of Supply for Goods

1. When Movement of Goods is Involved

Rule: The Supply of Goods under GST is determined by where the goods are delivered after movement.

Example:

- Scenario: A furniture manufacturer in Mumbai, Maharashtra, sells a sofa to a customer in Pune, Maharashtra.

- Movement: The sofa is transported from Mumbai to Pune.

- Place of Supply: Pune, Maharashtra.

- GST Applicable: Since it’s within the same state, CGST and SGST are charged.

Inter-State Movement Example:

- Scenario: The same manufacturer sells to a customer in Ahmedabad, Gujarat.

- Movement: Mumbai to Ahmedabad.

- Place of Supply: Ahmedabad, Gujarat.

- GST Applicable: As it’s inter-state, IGST is charged.

2. When There is No Movement of Goods

Rule: Place of Supply is where the goods are located at the time of delivery.

Example:

- Scenario: A machinery seller in Delhi sells equipment stored in a Delhi warehouse to a buyer in Delhi.

- Movement: The buyer picks up the machinery from the warehouse.

- Place of Supply: Delhi.

- GST Applicable: CGST and SGST are charged.

3. Goods Supplied on Board a Conveyance

Rule: Place of Supply is where goods are taken on board.

Example:

- Scenario: You buy a snack on a train traveling from Kolkata, West Bengal to Bhubaneswar, Odisha.

- Place of Supply: If the train stocked the snack in Kolkata, the Place of Supply is West Bengal.

- GST Applicable: IGST is charged because the supplier’s location and Place of Supply are in different states

Place of Supply for Services

1. General Rule

For Registered Persons:

- Rule: Place of Supply is the location of the recipient.

For Unregistered Persons:

- Rule: Place of Supply is the recipient’s location if available, otherwise, the supplier’s location.

Example:

- Scenario: A software company in Bengaluru, Karnataka, provides services to a registered client in Hyderabad, Telangana.

- Place of Supply: Hyderabad, Telangana.

- GST Applicable: IGST is charged.

2. Services Related to Immovable Property

Rule: Place of Supply is where the property is located.

Example:

- Scenario: An architect in Chennai, Tamil Nadu, designs a building in Goa for a client in Delhi.

- Place of Supply: Goa.

- GST Applicable: Since the supplier is in Tamil Nadu and Place of Supply is Goa, IGST is charged.

3. Performance-Based Services

Rule: Place of Supply is where the services are performed.

Example:

- Scenario: A car repair service in Jaipur, Rajasthan, fixes a tourist’s car from Punjab.

- Place of Supply: Jaipur, Rajasthan.

- GST Applicable: CGST and SGST are charged.

4. Training and Performance Appraisal

For Registered Recipients:

- Rule: Place of Supply is the recipient’s location.

For Unregistered Recipients:

- Rule: Place of Supply is where the services are performed.

Example:

- Scenario: A training firm in Pune, Maharashtra, conducts a workshop for employees of a company registered in Delhi.

- Place of Supply: Delhi.

- GST Applicable: IGST is charged if the ticket seller is in a different state.

5. Admission to Events

Rule: Place of Supply is where the event is held.

Example:

- Scenario: You buy a ticket for a concert happening in Mumbai, Maharashtra, but purchase it online from Kolkata, West Bengal.

- Place of Supply: Mumbai, Maharashtra.

- GST Applicable: IGST is charged if the ticket seller is in a different state.

Special Cases and Exceptions

1. Transportation of Goods

Rule:

- For Registered Recipients: Place of Supply is the recipient’s location.

- For Unregistered Recipients: Place of Supply is where goods are handed over.

Example:

- Scenario: A logistics company in Gujarat transports goods for a registered business in Rajasthan.

- Place of Supply: Rajasthan.

- GST Applicable: IGST is charged.

2. Telecommunication Services

Rule: Place of Supply is the billing address of the recipient.

Example:

- Scenario: A mobile service provider based in Delhi bills a customer whose billing address is in Haryana.

- Place of Supply: Haryana.

- GST Applicable: IGST is charged.

3. Banking and Financial Services

Rule: Place of Supply is the location of the recipient as per records.

Example:

- Scenario: A bank in Mumbai provides services to an account holder residing in Bengaluru.

- Place of Supply: Bengaluru, Karnataka.

- GST Applicable: IGST is charged.

Import and Export of Goods and Services

1. Import of Goods

Rule: Place of Supply is the location of the importer.

Example:

- Scenario: A company in Chennai, Tamil Nadu, imports electronics from China.

- Place of Supply: Chennai, Tamil Nadu.

- GST Applicable: IGST is levied on imports.

2. Export of Goods

Rule: Place of Supply is the location outside India.

Example:

- Scenario: A textile exporter in Surat, Gujarat, ships fabrics to France.

- Place of Supply: France (outside India).

- GST Applicable: Exports are zero-rated, so no GST is charged.

3. Import and Export of Services

Import of Services:

- Rule: Place of Supply is in India if the recipient is in India.

Export of Services:

- Rule: Place of Supply is outside India if certain conditions are met.

Example (Export of Services):

- Scenario: An IT company in Bengaluru provides software development services to a client in the USA.

- Place of Supply: USA (outside India).

- GST Applicable: Service is zero-rated; no GST is charged.

Impact on Input Tax Credit (ITC)

Correct determination of the Place of Supply is crucial for claiming ITC.

- Correct GST Charged: Ensures that you can claim ITC without issues.

- Avoids Mismatches: Wrong Place of Supply can lead to mismatches in GST returns and potential audits.

- Compliance: Helps maintain compliance and avoid penalties.

Common Mistakes to Avoid

- Assuming Supplier’s Location as Place of Supply: Always follow the rules; the Place of Supply often depends on the recipient or the location of performance.

- Ignoring Special Provisions: Some services have specific rules (like transportation or telecommunication services).

- Incorrect Billing: Ensure invoices reflect the correct Place of Supply to avoid ITC issues.

- Overlooking Documentation: Maintain proper records of transactions and communications.

Real-Life Case Studies

Case Study 1: Online Consultancy Services

Scenario: Priya, a freelance consultant based in Kerala, provides online consulting to a client in Delhi.

- Place of Supply: Delhi.

- GST Applicable: IGST is charged.

Insight: Even though services are provided online, the recipient’s location determines the Place of Supply.

Case Study 2: Event Management Services

Scenario: An event management company in Jaipur organizes a wedding in Udaipur, Rajasthan, for a client from Mumbai.

- Place of Supply: Udaipur, Rajasthan.

- GST Applicable: CGST and SGST.

Insight: Since services are related to an immovable property (venue), the Place of Supply is where the event takes place.

- Why is Place of Supply Important?

- Place of Supply for Goods

- 2. When There is No Movement of Goods

- 3. Goods Supplied on Board a Conveyance

- 1. General Rule

- 3. Performance-Based Services

- 4. Training and Performance Appraisal

- 5. Admission to Events

- Special Cases and Exceptions

- 1. Transportation of Goods

- 2. Telecommunication Services

- 3. Banking and Financial Services

- Import and Export of Goods and Services

- 1. Import of Goods

- 2. Export of Goods

- 3. Import and Export of Services

- Impact on Input Tax Credit (ITC)

- Common Mistakes to Avoid

- Case Study 1: Online Consultancy Services

- Case Study 2: Event Management Services

Table of Contents

- Why is Place of Supply Important?

- Place of Supply for Goods

- 2. When There is No Movement of Goods

- 3. Goods Supplied on Board a Conveyance

- 1. General Rule

- 3. Performance-Based Services

- 4. Training and Performance Appraisal

- 5. Admission to Events

- Special Cases and Exceptions

- 1. Transportation of Goods

- 2. Telecommunication Services

- 3. Banking and Financial Services

- Import and Export of Goods and Services

- 1. Import of Goods

- 2. Export of Goods

- 3. Import and Export of Services

- Impact on Input Tax Credit (ITC)

- Common Mistakes to Avoid

- Case Study 1: Online Consultancy Services

- Case Study 2: Event Management Services

Start using OLAO today

- Get Paid Faster. Boost Cash Flow

- Powerful, automated core accounting

- Hands-free bank reconciliation

Frequently Asked Questions

You should issue a credit note and a revised invoice with the correct GST. Also, rectify the error in your GST return for that period.

For e-commerce, the Place of Supply rules determine the GST to be collected at source and the compliance requirements.

Not always. It depends on the nature of the service. For some services, it's the location of the supplier or where the service is performed.