Home » Accounting Dictionary – What are different types of accounts?

- TRENDING ARTICLE

What are Different Types of Accounts in Accounting? A Comprehensive Guide

Anurag Mittal

Anurag Mittal, CEO and Co-founder of Olao Books, is an expert in business finance and operations, with a focus on transforming accounting and payroll solutions for small and medium-sized businesses. As the Co-founder and former Head of Operations and Business at Vervotech, Anurag played a pivotal role in driving 10x revenue growth and leading the company to a successful acquisition.

Accounting can seem like a maze of numbers and jargon, but at its core, it’s all about keeping track of money. To do this effectively, accountants use different types of accounts. Understanding these accounts is crucial for anyone involved in finance, whether you’re a business owner, a student, or a budding accountant. So, let’s dive into the various types of accounts in accounting and demystify the process!

Table of Contents

ToggleWhat is an Account in Accounting?

Definition of Account

An account in accounting is a record that tracks the financial activities of a specific asset, liability, equity, revenue, or expense. Each account shows the balance and history of increases and decreases.

Importance of Accounts

Accounts help in organizing financial data, ensuring accuracy, and making it easier to generate financial reports. They are the building blocks of the accounting system, providing insights into the financial health of a business.

Classification of Accounts

A) Traditional Approach

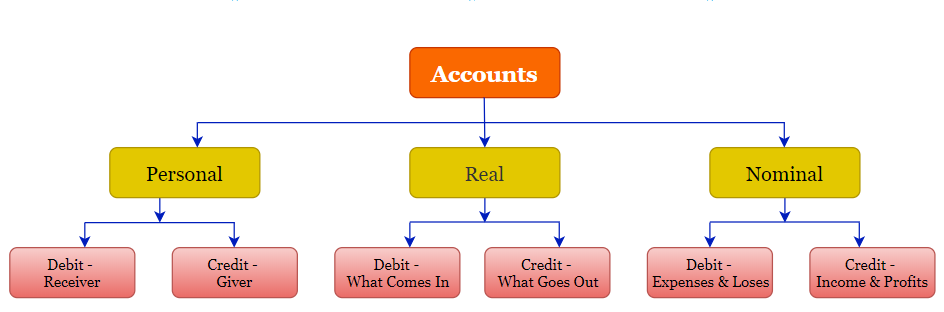

The traditional approach to classifying accounts divides them into three main categories: Personal, Real, and Nominal accounts.

B) Modern Approach

The modern approach classifies accounts into five types: Assets, Liabilities, Equity, Revenue, and Expenses. This method aligns with the accounting equation: Assets = Liabilities + Equity.

A) Traditional Approach – Account Categories

1. Personal Accounts

Definition

Personal accounts are accounts related to individuals, firms, companies, and other organizations. These accounts are used to record transactions with any entity.

Examples

- Individual Accounts (e.g., John’s Account)

- Firm Accounts (e.g., XYZ Traders Account)

- Company Accounts (e.g., ABC Ltd. Account)

Rules for Personal Accounts

The golden rule for personal accounts is: “Debit the receiver, Credit the giver.”

2. Real Accounts

Definition

Real accounts, also known as permanent accounts, represent assets and liabilities that are not closed at the end of the accounting period.

Examples

- Asset Accounts (e.g., Cash, Building)

- Liability Accounts (e.g., Loans Payable)

Rules for Real Accounts

The golden rule for real accounts is: “Debit what comes in, Credit what goes out.”

3. Nominal Accounts

Definition

Nominal accounts are temporary accounts that record income, expenses, gains, and losses. They are closed at the end of the accounting period.

Examples

- Revenue Accounts (e.g., Sales)

- Expense Accounts (e.g., Rent, Utilities)

Rules for Nominal Accounts

The golden rule for nominal accounts is: “Debit all expenses and losses, Credit all incomes and gains.”

B) Modern Approach – Account Categories

We should preface this headline by saying businesses can have a seemingly endless number of account types. And while that’s true, all those accounts fall under one of 5 account categories. This makes compiling the other account types easier for systematic review and retrieval.

The 5 primary account categories (also called real accounts) are as follows:

Once you understand how debits and credits affect the above real accounts, it will be easier to determine where to place your sub-accounts. Getting familiar with how debits and credits affect the different types of real accounts is important.

So let’s explore that now and see what kind of impact they have. Below is a handy chart explaining the effects that debits and credits have on each of the five primary account types.

Account Type | Debit Effect | Credit Effect |

Assets | Increased | Decreased |

Liabilities | Decreased | Increased |

Expenses | Increased | Decreased |

Income | Decreased | Increased |

Equity | Decreased | Increased |

1. Assets

Assets are what a business owns. They are resources with economic value that can provide future benefits. Assets can be divided into two categories:

- Current Assets: These are assets that can be easily converted into cash within a year. Examples include cash, accounts receivable, and inventory.

- Non-Current Assets: These are long-term investments that cannot be quickly converted into cash. Examples include property, plant, and equipment (PP&E), and intangible assets like patents.

Examples:

- Cash in hand

- Accounts receivable (money owed by customers)

- Inventory (goods available for sale)

2. Liabilities

Liabilities are what a business owes. These are obligations that need to be paid off in the future. Like assets, liabilities are also categorized:

- Current Liabilities: Debts or obligations due within a year. Examples include accounts payable, short-term loans, and taxes owed.

- Non-Current Liabilities: Long-term obligations not due within a year. Examples include long-term loans and bonds payable.

Examples:

- Accounts payable (money owed to suppliers)

- Short-term loans

- Mortgage on a business property

3. Equity

Equity represents the owner’s claim after all liabilities have been deducted from assets. It’s often referred to as the net worth of the business. In a simple equation, it looks like this:

Equity = Assets – Liabilities

Examples:

- Owner’s capital

- Retained earnings (profits reinvested into the business)

4. Revenue

Revenue is the income a business earns from its normal business operations, typically from the sale of goods and services. It’s crucial for tracking the business’s financial performance.

Examples:

- Sales revenue

- Service revenue

- Interest income

5. Expenses

Expenses are the costs incurred to generate revenue. They represent the money spent on the day-to-day operations of the business. Expenses can be divided into operational expenses and non-operational expenses.

Examples:

- Rent

- Salaries and wages

- Utilities

- Office supplies

Difference Between Personal, Real, and Nominal Accounts

Understanding the difference between personal, real, and nominal accounts is crucial for accurate accounting. Personal accounts relate to individuals and entities, real accounts to assets and liabilities, and nominal accounts to income and expenses.

Importance of Understanding Different Types of Accounts

Knowing the different types of accounts helps in accurate bookkeeping, financial analysis, and strategic planning. It ensures that financial statements are accurate and provides a clear picture of the business’s financial health.

Common Mistakes in Accounting

- Misclassifying accounts

- Failing to reconcile accounts

- Overlooking accruals and deferrals

- Ignoring internal controls

Conclusion

Understanding the different types of accounts in accounting is fundamental to managing finances effectively. Whether you’re tracking assets, liabilities, equity, revenue, or expenses, each type of account plays a crucial role in painting a complete picture of a business’s financial health. So, get to know these accounts, and you’ll be well on your way to mastering the art of accounting!

Table of Contents

Start using OLAO today

- Get Paid Faster. Boost Cash Flow

- Powerful, automated core accounting

- Hands-free bank reconciliation

Frequently Asked Questions

The three main types are Personal, Real, and Nominal accounts.

Proper classification ensures accurate financial reporting and helps in decision-making.

Current assets are short-term and expected to be converted to cash within a year.